Blog Layout

Mortgage Penalties

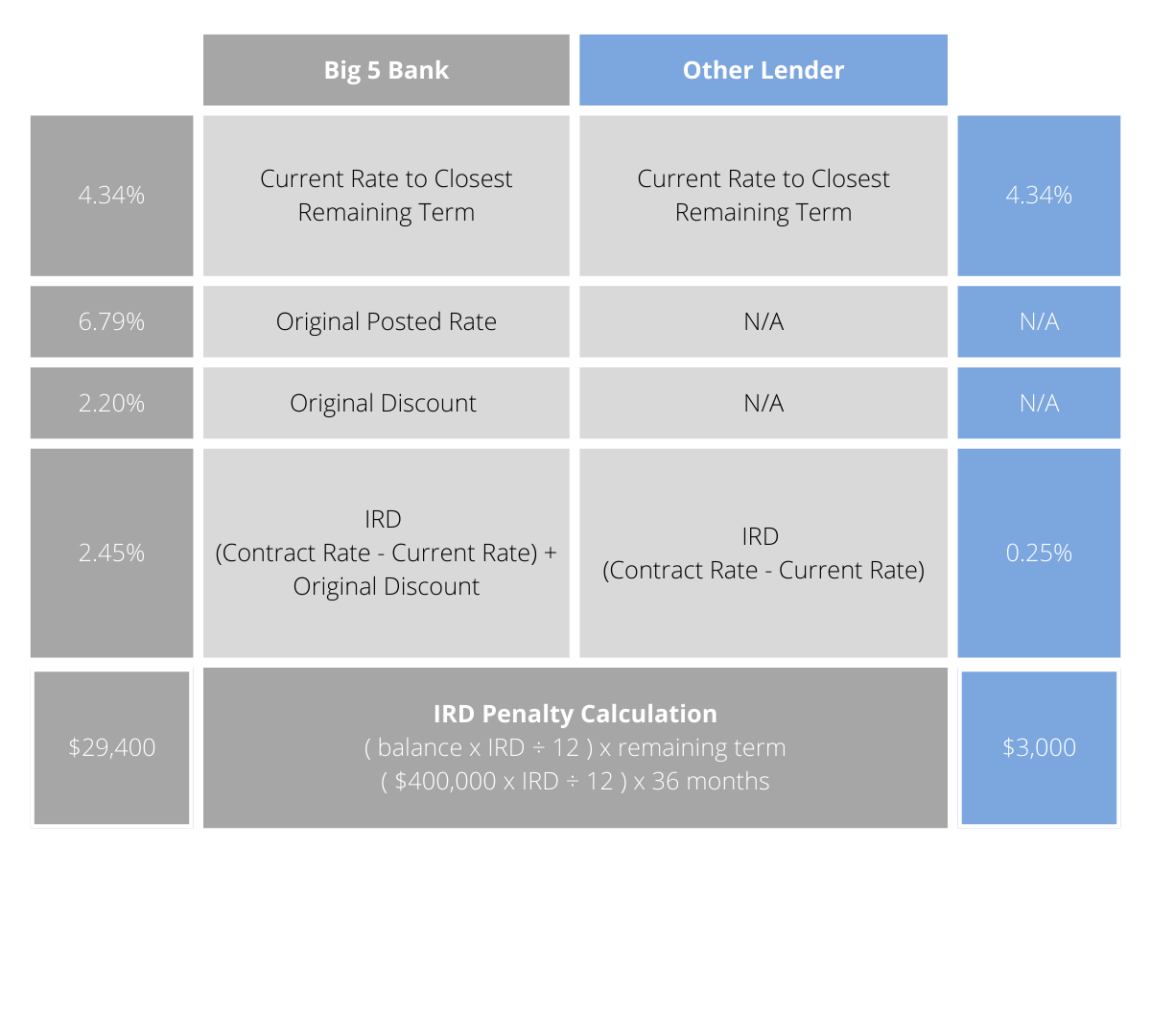

IRD PENALTY CALCULATIONS

How an IRD penalty is calculated varies between lenders, and the cost difference can be staggering!

Lenders like the Big 5 Banks offer discounts on their posted rates upfront. That “discount” can come back to haunt you, as it is used in the IRD penalty calculation. As a mortgage broker, we have access to other lenders where this is not a concern. No posted rates or discounts; what you see is what you get.

In this example calculation table, the original contract rate in both scenarios is 4.59%. At the time of breaking the mortgage the current balance is $400,000 with 3 years remaining.

The difference in IRD penalty calculations equals $26,400!

CONTACT US

VISIT US

#13 - 327 Prideaux Street

Nanaimo, BC V9R 2N4